Tesla ended production of the Model S and Model X in Q2 2026. Not because they ran out of demand. Because they needed the factory floor for something else.

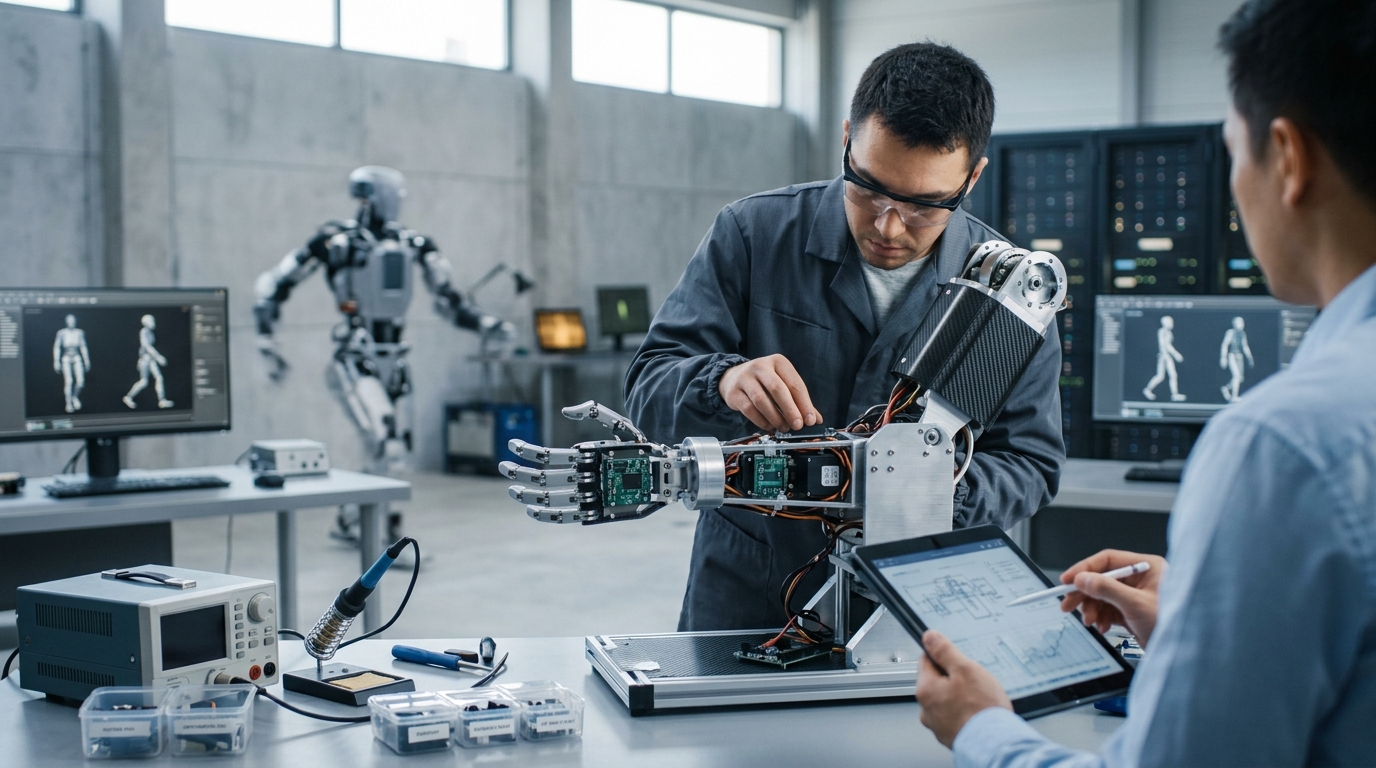

Optimus robots.

Think about that for a second. A company that spent fourteen years building two of the most iconic electric vehicles in history just retired both lines — and converted the Fremont factory to manufacture humanoid robots instead. Elon Musk called it giving the programs “an honorable discharge” as Tesla moves into a future based on autonomy. That’s not a press release. That’s a strategic identity shift.

The numbers behind the pivot are starting to matter. During Tesla’s Q1 2026 earnings, the company reported about $3.94 billion in net cash provided by operating activities. In the same quarter, Tesla’s GAAP gross margin was about 21.1% — the financial footing to fund an aggressive robotics buildout. Management has also discussed first-generation Optimus production lines being installed in Fremont with an intended annual capacity of 1 million robots. At Gigafactory Texas, Tesla has said a second-generation Optimus line is being prepared with a long-term target of 10 million robots per year.

Ten million units a year. Let that sit for a moment.

The third-generation model, Optimus V3, has been described in some robotics-trade coverage as featuring 37 joints — nine more than the prior generation — with improved dexterity and a walking speed up to 1.2 meters per second. However, Tesla has not published an official Optimus V3 spec sheet or a confirmed public production schedule. As of June 21, 2026, treat the “July to August 2026” large-scale production window — and the 2027 external commercial testing timeline — as tentative rather than company-confirmed.

Here’s the thing the market keeps getting tangled up on: it’s trying to value Optimus like a product line, when it’s probably better understood as a platform. The same way the iPhone wasn’t just a phone — it was a distribution system for everything that came after it. If Optimus scales at anything close to Tesla’s stated ambitions, it doesn’t just add a revenue stream. It rewrites what Tesla is.

The humanoid robotics market was estimated at roughly $4.3 billion in 2025. Projections push it toward $70 billion by 2032. That’s a 17x expansion window over seven years, driven by labor shortages, AI-native control systems, and cost curves that are dropping faster than most analysts modeled. Tesla’s manufacturing DNA — vertical integration, in-house chip design, real-world AI training data from its vehicle fleet — is arguably the most underappreciated advantage in that race.

The competition is real, to be fair. Figure AI has been reported as being in talks around a roughly $39–$39.5 billion valuation, and has discussed deployments with BMW. Apptronik disclosed a February 2026 Series A extension that brought its total Series A financing to $935 million (and total capital raised to nearly $1 billion), and it has partnerships with Mercedes-Benz and Google DeepMind related to embodied AI work. The humanoid space is crowded with serious money and serious engineers.

But most of those competitors are private. Retail investors can’t directly access Figure, Apptronik, or Agility Robotics through a standard brokerage account. Tesla, for all its complexity and controversy, is the one large-cap public company where humanoid robotics manufacturing is being positioned as a near-term priority — with Fremont capacity being repurposed from Model S/X and Tesla publicly describing dedicated Optimus capacity plans.

The risks aren’t small. Optimus contributes zero to Tesla’s current revenue. Production timelines have already slipped at least once from earlier targets into later timeframes. Musk’s estimates have a historical tendency to be optimistic. And Tesla’s core EV business is navigating its own headwinds — demand softness, margin pressure, brand noise tied to Musk’s public profile.

None of that makes this the wrong stock. It makes it a complicated one. The multiple you pay for Tesla today reflects the EV business, the energy storage business, the autonomy optionality — and somewhere buried in there, a robots business that could eventually be larger than all of them.

What I keep coming back to is this: converting a factory from Model S production to humanoid robot production is not a press release move. That’s capital, tooling, headcount, and manufacturing commitment. Tesla is already doing the thing most companies are still studying in a whitepaper.

The question isn’t whether robots are coming. It’s whether TSLA is the right vehicle for the bet. That answer probably depends on your time horizon — and your tolerance for holding through the noise while the production ramp matures. Full breakdown worth exploring before the next big Optimus milestone lands.